BBB study finds uneven laws and stolen data allow predatory payday loan companies and scammers to thrive.

Introduction

Predatory payday loan companies and scammers posing as legitimate companies rake in millions of dollars each year, despite best efforts from advocates and authorities to protect consumers. With the addition of online lending companies, the ever-complex web of small-dollar lending across North America has grown even thornier.

According to reports and complaints to Better Business Bureau (BBB) consumers lose out on hundreds and sometimes thousands of dollars amid complicated three-figure interest rates.

In one case of the thousands received by BBB, a consumer, Veronica in Dallas, Texas, took out a loan for $600. She fell behind on payments and the amount owed increased to more than $1,000. Veronica is now considering bankruptcy.

“I can’t afford payments,” she said. “I’m trying to pay but not double what the loan is.”

Scammers have found a home within the shadows of the industry as well, leveraging information stolen from legal payday loan companies to defraud unsuspecting people, leading to $4.1million in losses. BBB data itself shows a slight drop in these cases, but the Federal Trade Commission’s Consumer Sentinel data showed a 27% increase from 2019 to 2021.

This fraudulent activity takes on a few different forms, such as advance fee and debt collection ruses, but they share the characteristics of many scams tracked by BBB. Scammers pretend to be trusted businesses to convince their targets to send money or bank account information. And with reports of some victims being used as ‘money mules' to launder cash for fraudsters, it appears that organized crime is involved.

Information in this report was compiled from public records, BBB Scam Tracker reports, data from complaints registered at BBB and the FTC’s Consumer Sentinel program as well as interviews with victims, experts and regulators.

What to expect from legal payday loan companies and scammers impersonating them

Payday loan and advance fee scams

Scammers often pretend to be an employee of a legal, well-known payday loan company and target people down on their luck financially, according to reports compiled by BBB. Many victims believed the money they were promised would be as a timely lifeline.

In a typical payday loan scam, the fraudster uses a few different tactics:.

● They ask the customer for sensitive information, like bank accounts or Social Security numbers. Claiming the information is needed to deposit money, they can use this information to either steal money or sell data. They may even do a combination of these things.

● Scammers send money on an app like Venmo, Zelle or may use the victim’s real bank account. Much like the traditional bounced check, services like Venmo warn that strangers “send a payment to you, then contact you to say they sent it by mistake.” The scammer is actually taking advantage of the payment approval system and there may not have been any money sent. Eventually, the bank or service will reclaim that money, and the victim will have sent their own money to the fraudsters.

Advance fee loan scams function largely the same, but the scammers instead tell the victim they need to send a small fee to release the loan to their account. BBB has warned that scammers will sometimes “guarantee” the loan with a small fee. There is no loan, however. They ask for money in a form that is nearly impossible to recoup, like gift cards or wire transfers from places like Western Union. Once the scammers have their money, they disappear.

Victims told BBB they attempted to get these loans because they were already in debt due to payday loans. They talked about falling months behind on rent and other bills, because of the financial tolls these scams took.

Advance America and Lending Club were two of the most commonly impersonated companies in BBB’s Scam Tracker data. It has become such a problem that the companies themselves warn about impersonation scams on their websites.

In San Jose, Calif., Shirley received a call from a woman who said her name was “Lauren Green.” Shirley had qualified for a $5,000 loan from the West Point Lenders. To get her loan, all she needed to do was pay $535 as a fee. After doing so, Shirley was told by Green that another $535 was needed because her credit was not good enough. Now out $1,070, Shirley began to get suspicious. It turns out that West Point Lenders is similarly named to other financial institutions, but is a fake company. Green attempted to get more money from Shirley, but she realized she had been scammed. The phone number the scammer called from is no longer working.

International Association of BBB Research collected the data on susceptibility, which shows how likely someone complaining to the organization was to lose money to a scammer. To calculate the figure, BBB takes the number of complaints and checks it against how many of the reports actually lost money. In the case of advance fee loan scams, BBB found that victims were at high risk if contacted.

The monetary loss reported by consumers to BBB Scam Tracker likely under-represents the scope of the issue. FTC research finds less than 10 percent of fraud victims report their losses to BBB or law enforcement.

Those fighting fraud in Canada, like the Canadian Anti-Fraud Centre (CAFC), only keep data on advance fee scams, but the numbers are equally striking.

Figures from the Consumer Sentinel Network include consumer complaints submitted directly to the FTC and to 45 data contributors, including 25 State Attorneys General and all North American Better Business Bureaus. Consumer Sentinel data includes both fraud and other types of reports. Because BBB reports its data to the organization, there may be some overlap in the data listed in this study. An official at the FTC said that the “pandemic years” of 2020 and 2021 saw a huge influx of complaints in general. They attributed that spike to people having a better ability to complain while sheltering in their homes, and said reductions in 2022 don’t necessarily mean less scams.

Debt collection scams

The goal in debt collection scams is largely the same as payday loan and advance fee scams: convince unsuspecting people to hand over cash. The difference is in the tactics.

Scammers call people pretending to be debt collectors, saying they have unpaid fees or installments on a payday loan. In some cases, the fraudsters had information about the people, about past loans, phone numbers, addresses, emails, family members’ names and even Social Security numbers. Many told BBB that those personal assurances are what kept them on the hook during the scams.

While it is hard to know exactly where they receive the information in these cases, BBB found in at least one instance that hackers stole information from payday loan companies and posted it online for sale. That type of personal information makes it much easier for scammers to convince victims that they may have forgotten to make a payment on a loan and hand over money. Once they have convinced people, they will use similar methods to other scams, like asking for gift cards or money orders.

Fraudsters often use names that sound like law firms to convince consumers and make their threats sound more serious. A BBB investigation into BlackRock Legal Group found the supposed company sending mailers to people, saying they owed on a debt from Advance America, a real payday lending company. Advance America told the BBB that has no dealings with BlackRock, however.

A red flag in debt collection scams is the failure or inability to provide written confirmation of the debt, which should include the creditor’s name, amount owed and how to dispute the debt within 30 days of receiving the confirmation documents.

Chuck of Fort Collins, Colo., got a call one day from a stranger at a company called “DLS.” He was shocked when the scammer told Chuck there was pending legal action against him because of an overdue debt. The fraudster used a common tactic of giving little information, despite his questions about the amount owed. Chuck, afraid of getting into any legal trouble, sent them $5,000.

Legal payday loan companies

When it comes to legal payday loan companies, a web of laws, complicated interest rates and lobbying interests means that navigating the system remains complex and opaque.

Research, including complaints registered with BBB and BBB Scam Tracker reports, public records and expert opinion, show that despite efforts across the country to rein in the power of payday lending companies, many Americans are still trapped in an unexpected consumer debt cycle.

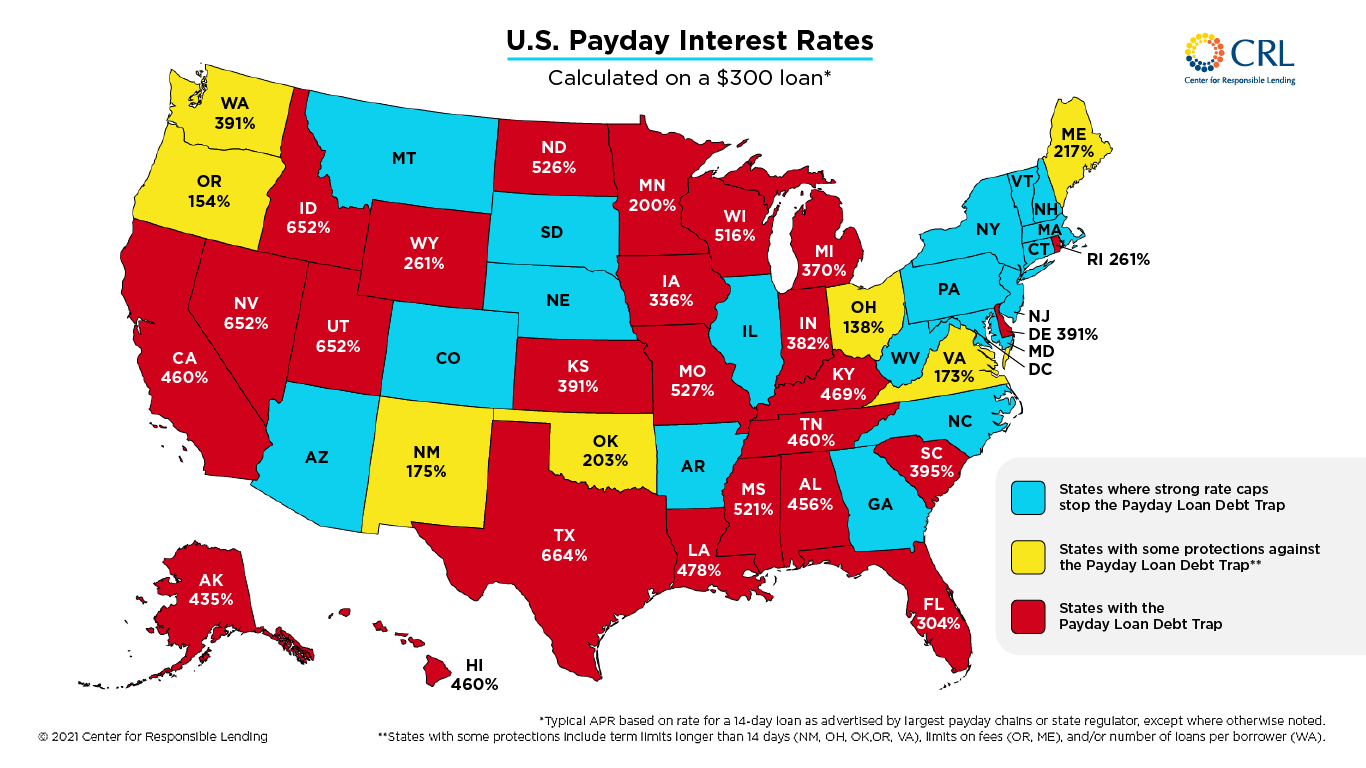

The way payday loans work is in the name. Borrowers needing small dollar loans sign on to pay back the money within a week or two, usually giving rights to automatically withdraw the cash from their account on pay day or writing a post-dated check. But the fees and interest rates are usually exorbitant. Payday loans operate in various forms in 32 states. These states allow triple-digit annual percentage rates (APR), with APRs in eight states above 400%, according to Pew Charitable Trusts. Laws in eighteen states either ban payday loan companies or cap interest rates so low that companies have stayed away.

Here’s how payday loan interest rates are calculated, according to InCharge Debt Solutions. Let’s say that a borrower is taking out a $375 loan with a very common finance charge of 15%. The actual interest paid is calculated by multiplying the loan amount by the interest charge ($375 x .15 = $56.25).

To figure out the APR, the math is a little more difficult. First, you divide the interest paid by the amount borrowed ($56.25/$375 = $.15). Then you multiply that by days in the year ($.15 x 365 = $54.75) and divide that by the repayment term. Two weeks is a common repayment length. ($54.75/14 = 3.9107). Finally, you multiply that by 100 for the true APR = 391.07%.

An advertised rate of 15% on a two-week payday loan sounds much more attractive than a loan with an 391.07% interest rate. The complicated math makes it hard for a consumer to convert the two-week rate. This often leads to borrowers taking out loans they can’t repay, letting interest pile up further.

A single working mother, Kristy took out a payday loan of $625 for rent in Chicago, Ill. The interest rates from the loan quickly overwhelmed her, and Kristy needed another $275 to deal with overdraft fees. Despite paying back about $650 over two months, interest has stacked so high that she has paid almost nothing on the principal.

In cases like Kristy’s, consumers need another loan to pay back the last one. In April, the Consumer Financial Protection Bureau (CFPB) published a report showing payday loan companies continue to steer consumers toward costly “reborrowing” programs rather than free extended repayment plans, which are required by most states that offer small dollar loans.

“In Washington state, which has perhaps the most borrower-friendly extended payment plan, the usage rate is a small fraction of all payday borrowers, 13.4%. States, such as Florida, with more restrictive requirements, have even lower usage rates,” CFPB wrote in a press release.

When consumers don’t or can’t take advantage of these repayment plans, they sometimes have their loans automatically “rolled over” into a new one with a new set of associated fees.

Let’s do a little more math to show how rollovers work. For the $375 loan with a 15% finance charge mentioned earlier, the total amount owed on the original loan is $431.25. The consumer now has the same finance charge of 15% applied to their total loan of $431.25, which comes out to $64.69. The borrower now almost owes $495.94. As InCharge puts it on their website: “That is how a $375 loan becomes nearly $500 in one month.”

Wanda is a resident of Forest Park, Ga. She wanted to build her credit and believed payday loans were a good way to do so. Soon after, she had taken out a loan for $1,000. Buried behind all of the fees and paperwork, her true interest rate was nearly 450%. She soon regretted the decision. “Older people and fixed income citizens like myself should never do business with this type of company,” Wanda said. “They charge you every two weeks, and it adds up to about $400.00 to $600.00 a month to pay back such a small amount.”

Military members have extra protections due to the Military Lending Act (MLA), which caps loans for service members at 36% APR along with a host of other assurances. The law states that an MLA certificate may be needed to prove enrollment in the military when asking for a loan.

Several states have followed the military’s lead in pushing for a 36% cap. As of March, 18 states used that benchmark as their cap and three more were considering legislation of ballot measures, according to American Banker. CNBC also wrote that major banks told Congress last year that they weren’t opposed to capping consumer loans at that level.

“The Predatory Loan Prevention Act will substantially restrict any entity from making usurious loans to consumers in Illinois,” Illinois Gov. J.B. Pritzker said to CNBC in 2021 after the state capped loans at 36%. “This reform offers substantial protections to the low-income communities so often targeted by these predatory exchanges.”

Not only do customers end up spending hundreds of dollars to borrow, they don’t realize the fees and interest rates are calculated on a short-term basis, rather than annual interest rates that most consumers know well. While completely legal, this leads to situations like Wanda’s.

With the addition in the last decade or so of online lenders, payday loan companies have found new ways to reach consumers. These companies are supposed to follow each individual state's rules, according to Consumer Federation of America. Most do, though some have been prosecuted in states like Virginia, where ABC 8 reported that a company was illegally giving loans online.

BBB has warned consumers that TikTok and Meta (owner of Facebook and Instagram) have rules restricting advertising payday loans on their platforms, though companies have found ways around them. There are instances of companies claiming to offer interest free or no-fee loans but charging customers nevertheless. Many use deceptive language like “fee or tip” when it is really an interest rate.

Older consumers and those on Social Security benefits are at extra risk of getting trapped in a payday loan debt cycle, according to AARP, because these populations are often already cash-strapped and any emergency expenses could tip their finances over the edge.

Canadian citizens have wide access to payday loans as well. Crushing interest rates exist throughout the provinces except for Quebec, which capped annual interest rates low enough to effectively ban the industry, according to The Globe and Mail. In the rest of the country, borrowers face interest rates as high as 652% in places like Prince Edward Island.

Darryl in Nova Scotia told BBB that he paid off his loan in full in October 2021, but the payday loan company that he used ended up charging him again. Because of the unexpected charge he didn’t have the money for, the payday loan company then charged him a non-sufficient funds fee on top of the unauthorized charge.

The payday loan industry members have pushed back on the rough categorization of their businesses, saying customers are happy with payday loans and recommend them to others.

Financial academics have also testified in front of Congress, saying “small-dollar credit products help them deal with volatile incomes and unforeseen expenses. The choice for these consumers is between using small-dollar credit products, or simply going without needed goods and services.”

While the assertion about access may be correct, legal aid and advocates pushing to regulate the industry say their application of the system remains predatory.

“Since the late 90s, we’ve seen this wild west type of payday lending,” said Dana Sweeney, a statewide organizer for Alabama Appleseed Center for Law & Justice, a nonprofit that compiled information on payday loans. “Currently, we are driving at 90 miles an hour with no guard rails.”

Sweeney said the varying interest rates in different states illuminate the flaws in our current regulatory landscape. Payday loan companies often argue that lowering rates would drive them out of business. But in states like Alabama, payday lending companies charge interest rates above 400%, Sweeney said. In other states, those same companies have much lower interest rates yet remain immensely profitable. “I am not persuaded by the argument from the payday loan industry,” he said.

Warnings abound, but scams and predatory companies remain successful

Scammers

Like most scams BBB has exposed, these swindles are a part of a vast network of attempts to con people out of their money. Scam Tracker reports show that people didn’t always sense a scam right away, but once they did, they were able to either hang up the phone or quit interacting with the fraudster on the spot, saving themselves hundreds, if not thousands, of dollars.

Consumers facing financial hardship are especially vulnerable to this type of scam. Many sought out payday or short-term loans, and the scammers use that mindset to exploit them. Dozens of reports to BBB –cited the necessity of the alleged loans, and how the scam left them far behind financially.

Jill of Ohio., told BBB how she applied online for an emergency loan that was offering $3,000 and reasonable terms. In a moment she now regrets, Jill turned over her banking information, which the scammers said they needed to send the money. Before she even realized, they were moving money out of her account. “I now owe 3 months of back rent,” she said. “I now face eviction.”

A BBB investigation found scammers will often change names to avoid scrutiny. One example saw an operation now called Delight Loans switching names every half year or so from titles like Victory Finance LLC, Consumer Needs, E Capital Finance, Saga Finance Co./Chicago, Sunrise Loans, Aviator Loans.

Concerns about legal payday loan businesses abound

Legal businesses are governed by a strict set of rules in some states, while other states allow payday lending companies almost complete control of their interest rate terms.

More than half of the country allows three-digit interest rates, according to Pew. Texas, Idaho, Nevada, and Utah have an average interest rate on payday loans above 500%. Missouri has a cap of nearly 2000%, with the next closest being around 600%.

For years, legal advocates and grassroot campaigns to curb payday lending have sought to cap interest rates and borrowing amounts. They have had some success, and studies have shown that payday loans cost four times more in states with fewer consumer protections. Industry experts claim these loans are not only needed by consumers, but that they willingly enter them as well.

What consumers tell BBB is something advocates have known for years: consumers are often fooled by payday loan companies' use of weekly, biweekly or monthly interest rates instead of annual percentage rate (APR). Credit cards, for example, use an APR rate. These are often in the 10-20% range, though they vary according to many factors. When consumers go into a payday loan company, they are usually presented with a similar interest rate of 15 percent. What's the catch? Those credit card interest rates are compounded annually, while the payday loans are much shorter, meaning the effective rates are often in the range of 390% annually, according to the Center for Responsible Lending.

{kind=link}

“Payday lenders often describe the cost of their loans in terms of fees or simple interest rates. Responsible lenders readily disclose the APR on their loans, aligned with the Truth in Lending Act,” Responsible Lending wrote in a press release. “They are not afraid to let their customers compare the costs of their loans to other loans in the market. Tellingly, payday lenders often object to having to disclose the APR of their loans.”

April from Carbondale, Ill., has felt the sting of hidden interest rates, telling BBB that over the course of a month, her balance owed ballooned from $430 to $818.

Interest rates aren’t the only thing consumers have hidden from them. Fees for different services often stack-up as well, increasing the debt owed.

Miguel in Torrance, Calif. was surprised to the repeated finance fees every few weeks as he extended his loan and worked to pay it off. After six weeks, he realized he had paid $900 on a $750 loan and had paid nothing but interest and fees.

Lending on the internet has complicated the issue. The government has ruled that states have final say over their lending, but that hasn’t stopped some companies from continuing to work with borrowers beyond the law. In some cases, consumers were charged 600% interest rates, according to ABC 8.

A number of complaints to BBB about payday loans involve companies on tribal land. News organizations like The Intercept and Al Jazeera America have shown instances of lenders using Native American tribes and sovereignty as a shield to continue to churn out predatory loans, despite the fact that courts are cracking down on the practice. But as Kansas City’s The Pitch wrote, business owners seeking to exploit consumers are doing it from all over the country.

Consumers faced with mounting debt have a steep hill to climb, but there are solutions. Several nonprofits, like the previously mentioned InCharge, help consumers make a plan to tackle their debts, make a budget and avoid future traps. Still, the FTC says on their website that people need to be wary as there are fees associated with services like InCharge, and there are many unscrupulous actors in that field as well.

The FTC has laid out several questions to ask when seeking out credit counseling:

● What services do they offer?

● Is there free information?

● Do they offer help making long-term plans?

● What are the fees? What if I fall behind on the fees?

● Are they licensed?

A few companies top the complaints to BBB about payday loans

Several legal payday companies triggered BBB’s radar after many complaints about unfair business practices like deceptive interest rates and automatic withdrawals. While some companies received one or two complaints, others have racked up hundreds of disgruntled customers over the last three years.

Speedy Cash topped BBB’s list of payday loan complaints. Until recently, Speedy Cash was owned by CURO Group. The Wichita, KS, company received more than 400 complaints, double the number of complaints against the next closest company during that time. Customers talk about a pattern of complaints: their bank accounts were overdrawn even though the company knew they didn’t have the funds, that Speedy Cash failed to remove old debts from credit reports and that opaque contract details led to confusing situations.

Donald, a customer in Pulaski, Tenn., told BBB that he doesn’t understand why he can’t get a lower payment amount approved or make any progress on his loan with Speedy Cash.

“I’ve been paying on this account for two years now it seems to never go down the account is always the same balance,” he said. “They won't work with me to lower payment. They tell (me) the account goes in collections if I don't pay full monthly payment.”

In May, Speedy Cash was acquired by Community Choice Financial, an Ohio-based lender. Prior to being contacted for the study, Community Choice entered into an agreement with BBB to address all past complaints, reach out to customers and work to eliminate any repeated patterns.

Executives also told BBB they train employees on best practices to ensure that no one is misled when taking out a loan. The company, unlike many other payday lenders, states its interest rates in APR form. It also has a no-fee, extended repayment plan in all states it serves, a step further than required by regulations.

Leadership at the company said anyone with a question about a previous unresolved Speedy Cash loan should reach out to the company’s toll free line, which now routes to Community Choice.

While Speedy Cash was the most complained about company to BBB over the last three years, many others had hundreds of reports. QC Holdings, which operates a number of branches all throughout the country under various names like Lend Nation, Quik Lend and CheckSmart, had a smattering of complaints at its various branches.

In addition, several tribal lenders, which have come under scrutiny for hiding their ties to the greater payday loan industry, repeatedly appeared on BBB’s complaint list.

Ashley in Omaha, Neb., was exploring a loan through a tribal lender when she realized that her $500 loan would have $1,000 in interest and fees . She never agreed to accept the loan, but it was deposited into her account anyway and payments were deducted automatically.

BBB also found at least one instance of hackers stealing information about payday loan customers and selling it online. On forums for selling databases of this sort, scammers post a fraction of their database as proof of its legitimacy. BBB saw a mix of 200,000 entries about payday loan customers. A huge cache of personal information was included for each of the people including:

● Full name

● Address

● Phone numbers

● Terms of loans

● Home details such as ownership or rental and monthly payment

● Job title

● Best hours to contact

● Social security number

● Routing and account numbers for bank

Complaints to BBB’s database about several companies suggest the issue is more common than this instance, and news reports indicate similar breaches have happened several times throughout the years.

Actions taken to address the problem

Since 2016, the CFPB has pursued payday lending companies with a series of rules that seek to map out abusive practices and curb them.

One rule regulates lenders with interest rates higher than 36% per year, a figure championed by advocates against predatory lending. That number was touted as a goal by the Obama Administration, according to NPR, which said the CFPB rules would be the “end of predatory lending.” The Trump Administration rolled back those rules, however, NBC wrote at the time. Industry lawyers and lobbyists have fought back, arguing that a recent Supreme Court ruling may invalidate some of those rules. Advocates aren’t convinced, Pyments.com wrote.

States are free to take the matter into their own hands and many have. More than a dozen states introduced legislation to regulate payday loans last year.

When it comes to scams, laws can only go so far. Many state governments — Washington, New York and Minnesota — have attempted to educate consumers and have warnings and tips for avoiding payday and debt collection scams. Payday loan companies like Speedy Cash and Advance America have written warnings about scams, describing the ways that they will and will not attempt to solicit consumers.

Prosecutions

There has been no shortage of legal action taken to curb payday lending and scams surrounding it, as awareness of practices has grown over the years and prosecutors of all stripes have sunk their teeth into the cases.

Charles Hallinan, a Pennsylvania businessman known as the “godfather of payday lending,” was sentenced to 14 years in prison after a jury found him guilty of racketeering conspiracy, mail fraud and wire fraud. His victims were said to have numbered in the hundreds of thousands, and Hallinan was ordered to pay back $2.5 million in fines.

In another case, race car driver Scott Tucker, whose online payday lending companies included Ameriloan, Cash Advance, OneClickCash and Preferred Cash Loans, was sentenced to 16 years in prison after he was found to have illegally been running a $3.5 billion payday loan company. Tucker, along with his co-defendant, came up with a scheme where they failed to inform customers of the actual terms and pulled money from people’s accounts to only pay interest on their loans, leaving the principal to accrue more interest.

The government’s ability to go after people like Tucker was weakened last year, however, when the Supreme Court ruled that “the agency overstepped its authority in its practice of seeking court orders to make fraudsters return money improperly obtained from consumers in the form of restitution or disgorgement,” according to Reuters. Still, the agency continues to send out redress payments to some of those affected.

The CFPB is currently suing ACE Cash Express for concealing no-fee repayment plans meant for consumers that failed to pay back their loans on time. The organization said it has amounted to at least $240 million in fees for the company. “Deception and misdirection allowed ACE Cash Express to pocket hundreds of millions of dollars in reborrowing fees,” CFPB said in a press release. “Today’s lawsuit is another example of the CFPB’s focus on holding repeat offenders accountable.”

In a positive resolution for consumers, the FTC announced in August that it is sending more than $1 million to nearly 2,000 people defrauded by a debt collection scheme where consumers were tricked into paying for payday loan and other debts they didn’t owe. The defendants in the case said they were from GAFS Group, Global Mediation Group, and Mediation Services while pretending to be attorneys that sought money for debts. They threatened to take legal action against those who didn’t pay.

The FTC is also sending $9.7 million to nearly 62,000 consumers who were charged hidden fees by Lending Club. The commission sued Lending Club in April 2018 “charging that the company falsely promised loan applicants that they would receive a specific loan amount with ‘no hidden fees,’ when in reality the company deducted hundreds or even thousands of dollars in hidden up-front fees from the loans.”

he Supreme Court ruled last year that the FTC does not have the power to seek monetary relief for consumers in court, though the commission is still able to distribute the money in the GAFS case. The FTC has urged Congress to reinstate those powers through legislation.

Tips for consumers

● If you miss your payment on a loan, check to see if your state has a no-cost extended repayment plan.

● The FTC regulates for how debt collectors can contact consumers, when they can reach out and what types of debts are covered under the law.

● No company will require an advance fee for a loan. Any fees and interest will either be taken out of the sum of the loan or charged to be repaid with the loan. If they ask for money to “release the loan” or “for bad credit” or “for insurance” that’s a scam.

● Whenever any company, legitimate or not, tells you that you have a debt, you should ask for written confirmation of the debt. Companies are legally required to do this, and it should put the brakes on any debt collection scam before it gets off the ground.

● Ask for the company’s name. Do a Google search and learn more about them. Don’t succumb to high pressure tactics, because any legitimate company will want your business, whether it is today or tomorrow. If you can’t find any information, that is a red flag. Sometimes scammers have fake websites, so the presence of one is not a guarantee that you are safe.

● If you get an email about a payday loan, check the info after the @ sign. Legitimate companies usually don’t send messages from a Gmail or Yahoo account. Again, this is not a foolproof method though, as scammers can spoof their emails or even steal passwords to gain access to legitimate ones.

● Never hand over any personal information until you are 100% certain that there is no scam.

● Real payday loan companies are unlikely to call you to offer a loan. As tempting or needed as the money may be, just hang up if you receive a call. You can find a branch near you if you decide you want to move forward with one of the loans.

● Read the terms and conditions of the loan. If it isn’t clear, ask for a copy and have someone help you go through it so that you can really know what you are paying.

● Military members have additional protections. The Military Lending Act caps loans at 36%. Anything higher than that for servicemembers is illegal.

● When seeking credit counseling, always ask these questions before paying for services

● What services do they offer?

Is there free information?

● Do they offer help making long-term plans?

● What are the fees? What if I fall behind on the fees?

● Are they licensed?

How to report cases

● If you are the subject of fraud, there are many avenues to report your case:

● Federal Trade Commission (FTC) - ReportFraud.ftc.gov

● Canadian Anti-Fraud Centre (CAFC) - Online or by phone at 1-888-495-8501

● State Attorneys General can often help. Find your state Attorney General’s website to see if you can file online.

● If you have an overdue payment on a payday loan, the Consumer Financial Protection Bureau may have resources to help you set up a payment plan.

Recommendations for regulators

● Cap payday loans federally at 36%, taking cue from the Military Lending Act and the 18 states that have already done so.

● Continue to make consumers aware of no-fee, long-term repayment plans when they fall behind on loans.

● Require small dollar lenders enact some sort of financial test to ensure borrowers can pay back their loans.

● Extend the minimum repayment time to at least one month.

● Encourage credit unions and other established lenders to make lower-interest small dollar loans available to their existing customers.

● Support the CFPB push to require Zelle, Venmo and other online cash services to repay those affected by fraud.

● Enact legislation in Congress to restore the FTC’s power to seek monetary damages in federal court.